Palladium Below $1,000-

Palladium Below $1,000-

What does the future hold?

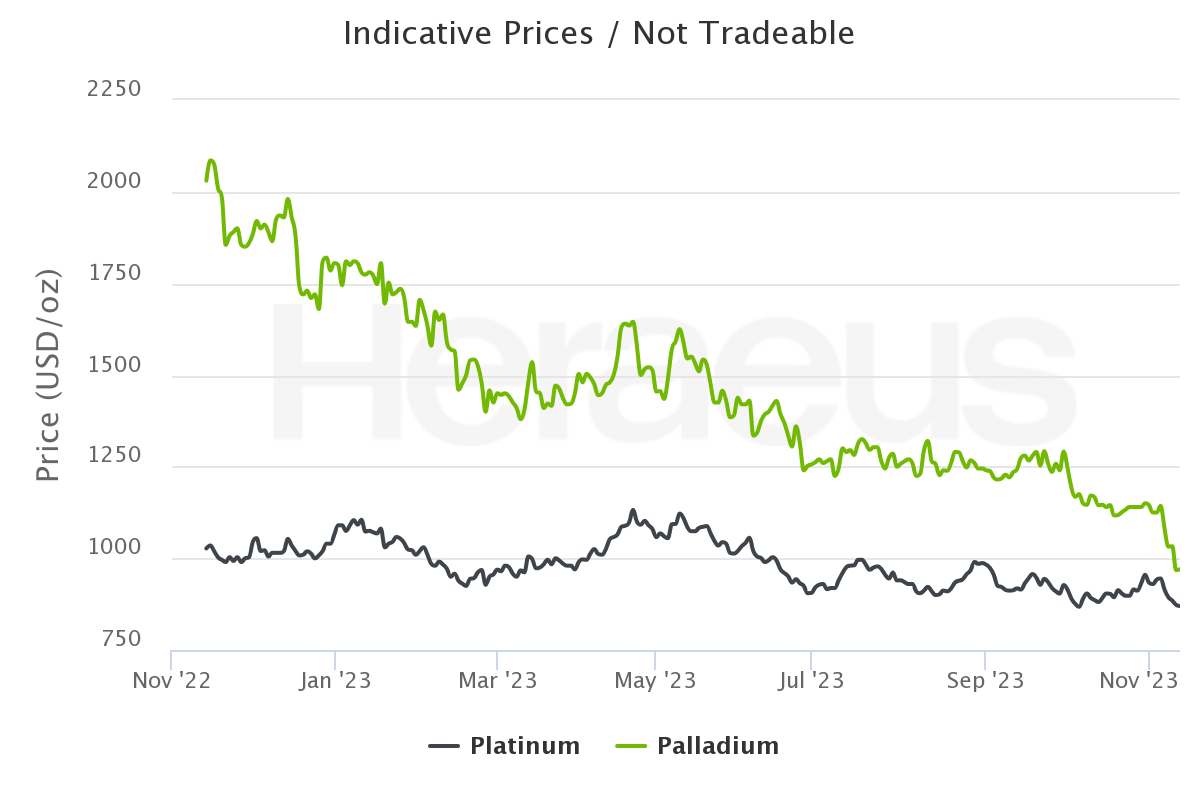

Palladium reached a feverish all-time high in March of 2022 of over $3000 per ounce on the back of the Ukraine-Russia conflict. The initial jump was after a correction that had seen it come down to about $1700 from the high of May 2021 when it previously neared the 3k mark.

What caused the initial decline from May of 2021 was the inability to produce autos caused by the semi-conductor shortage. After that it began to become apparent that a robust recovery was not going to be on its way due to a weakening global economic environment. This coupled with the increased supply of palladium from spent auto catalyst recovery and an increase of adoption of electric vehicles combined to put a preponderance of negative pressure on this market.

Markets though have a way of correcting themselves. The problem is timing and costs. With these low prices, which incidentally have not occurred in a vacuum as both rhodium and platinum prices have been suffering from the same tailwind, supply will change.

Lower commodity prices will put pressure on the Platinum Group Metals mining industry as their profitability is suffering a major collapse after the buoyant prices they had experienced during the pandemic. Simply put, many of the operations will become untenable and to remain profitable they will need to put the brakes on production. This will cause much pain and suffering for those working in the sector, but it beats operating at a loss and going out of business.

Yet, all is not doom and gloom. The BEV market will begin to hit its own walls of resistance as mineral supplies, environmental and humane concerns of their production will begin to slow production. Demand for Auto Catalyst will continue, and the major benefactor is the platinum market which is expected to see growth in this sector from the adoption of more 3-way catalyst as well as the new energy sector of the Hydrogen economy which is expected to grow the demand.

Though as my friends at SFA Oxford point out the possibility of prices going as low as $400 exists, it is more likely we will settle closer to the $800-$900 price level as supplies adjust to market price levels. Platinum will hopefully compensate for some as the market growth begins to materialize and we could easily expect prices at the $1500 level or higher in the next few years.

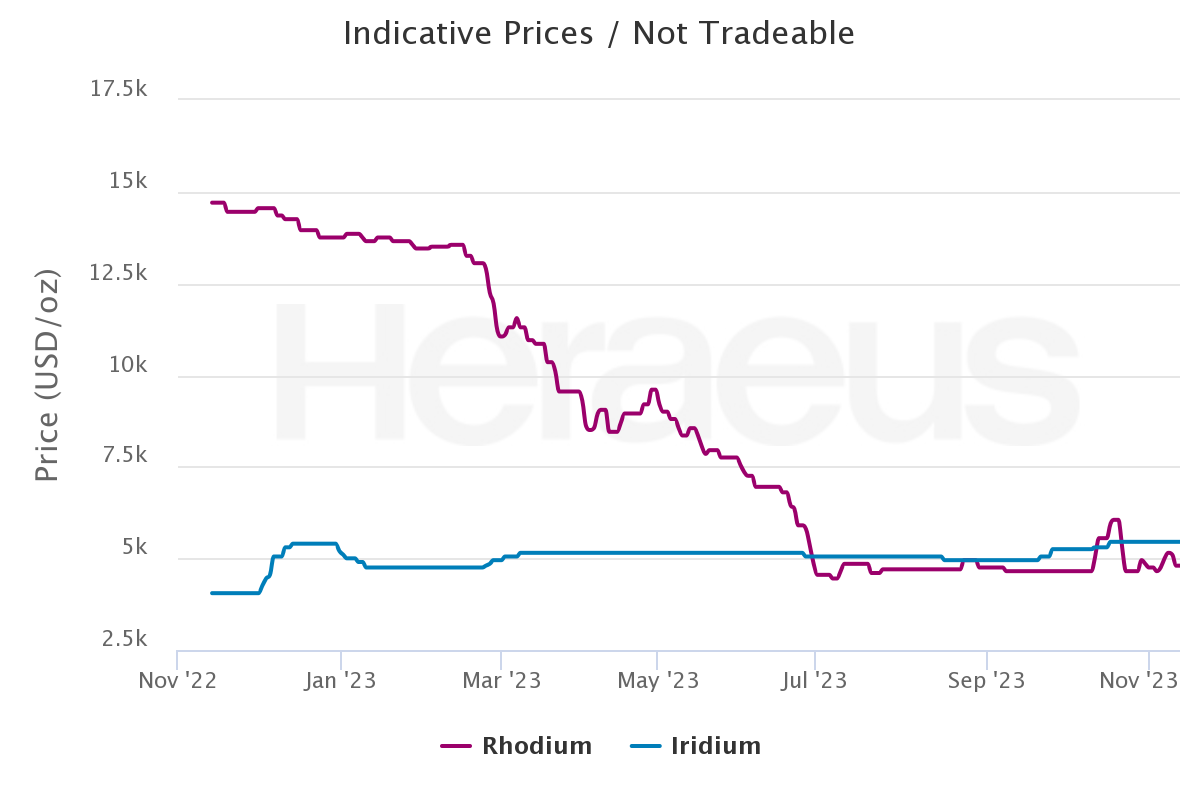

Of course, this does not come close to making up for the collapse of rhodium ($15,000 down to $4,000) and palladium prices, but Iridium and Ruthenium may also begin to carry some of the weight in the future. Market pundits seem to be quite bullish on iridium due to its most important function as a catalyst for PEM electrolyzers for hydrogen production.

The world, its demands and needs are always changing. Keeping on top of what is happening is often the most important factor in surviving any outcome. Most importantly, is working in good faith, for the benefit of all and all eventualities will work themselves out.

Remember the Telex, CDs, VHS and Fax machines? Change is inevitable.